American Cities With the Highest Debt-to-Income Ratios in 2022

For much of the COVID-19 pandemic, favorable financial conditions for many middle and upper-income households have brought a rush of new homebuyers into the real estate market. In 2020 and 2021, increased savings rates and government stimulus allowed millions of people to pay down debts from credit cards, student loans, and other consumer borrowing, while more recently, a tight labor market has helped boost wages. Both of these factors have helped prospective homebuyers improve on one of the key metrics that mortgage lenders consider when evaluating mortgage applications: the debt-to-income ratio.

The debt-to-income ratio is calculated as an individual’s monthly debt payments divided by their monthly income. As regular debt payments increase relative to income, an individual’s ability to pay debts while also covering their other expenses becomes more challenging. For that reason, lenders evaluate debt-to-income ratios when approving loan applicants to ensure that borrowers will be able to make payments reliably.

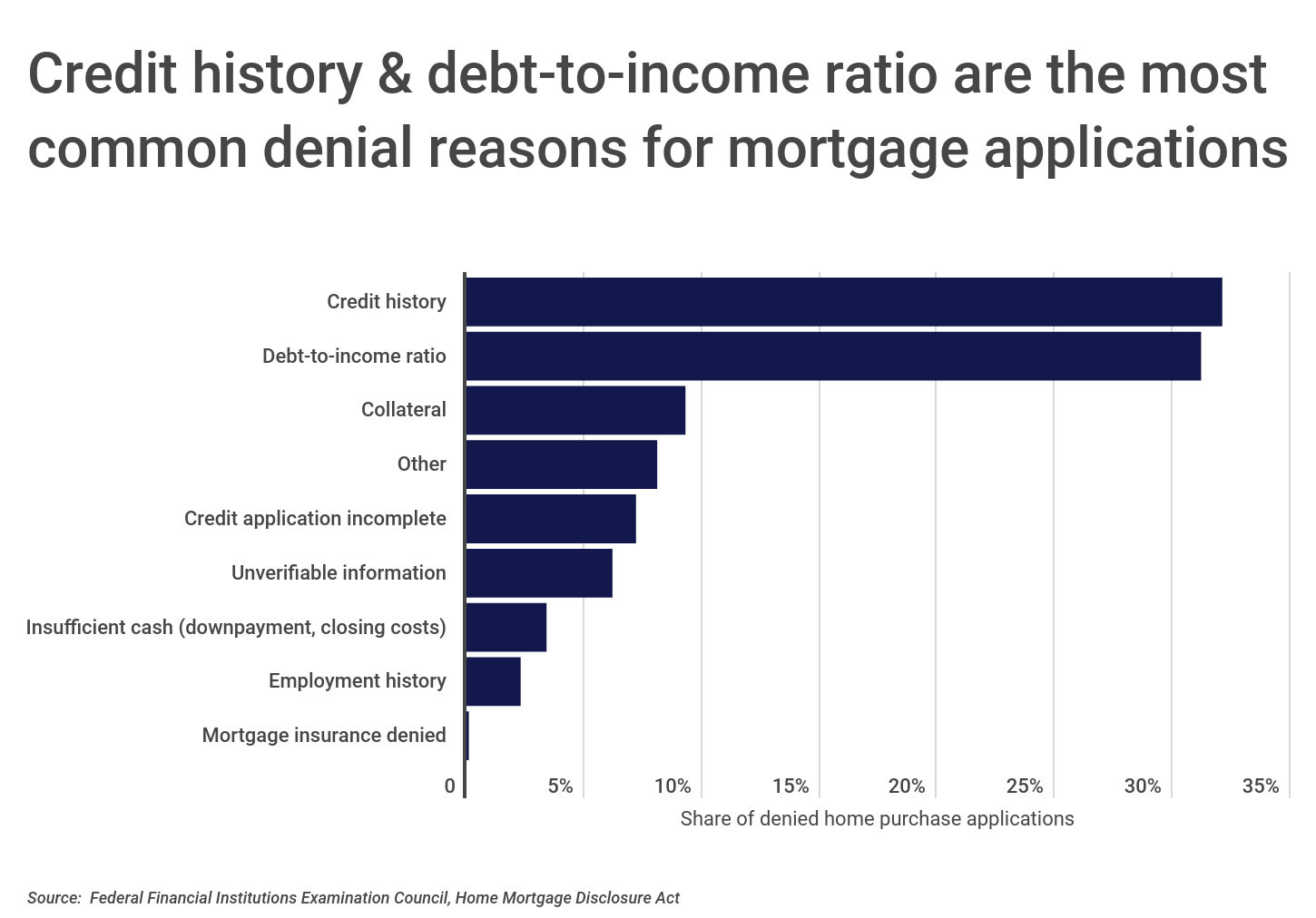

Debt-to-income ratio is especially important for mortgage approvals. Housing costs are the most significant regular expense for most households, so lenders want the assurance that an applicant’s debts and income level will not limit their ability to make payments on a home loan. According to data from the Home Mortgage Disclosure Act, 31.2% of mortgage applications are denied due to the applicant’s debt-to-income ratio. Debt-to-income levels trail only credit history (32.1%) among leading reasons for home purchase loan denials.

RELATED

Homeowners planning on an extensive remodel should make sure their home is covered by an adequate builders risk policy. Builders risk insurance covers the home and other structures on the property while under construction.

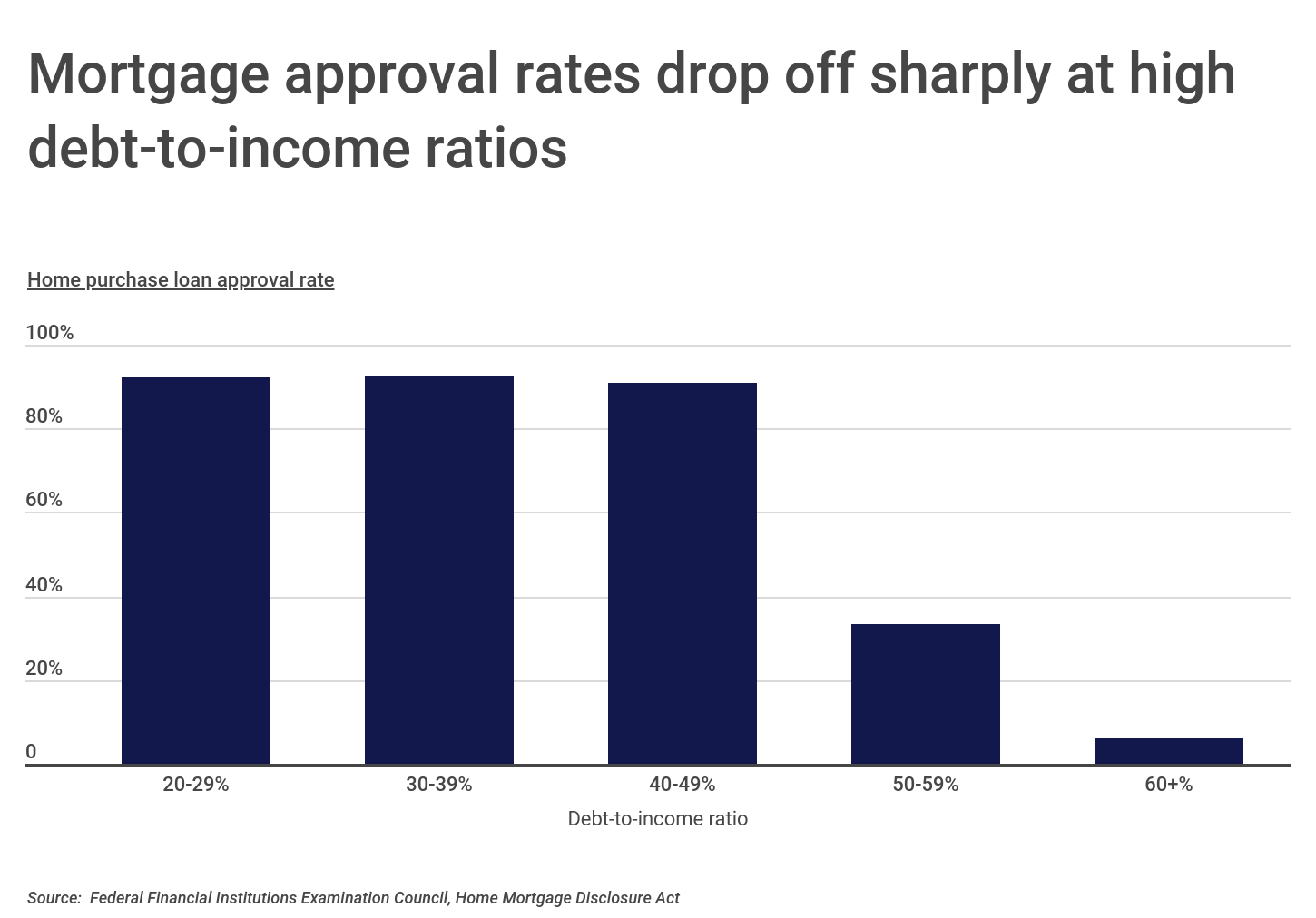

Lenders may vary in what they view as an acceptable debt-to-income ratio for different applicants, but one key threshold in the industry is a 43% debt-to-income ratio. The 43% figure is significant because it is the highest level that a borrower can have while receiving a Qualified Mortgage, a federal designation that limits risky loan terms for borrowers. Mortgage approval rates drop off significantly when applicants’ debt-to-income ratios rise much above that level. More than 90% of loans are approved with applicant debt-to-income ratios of 49% or less, compared to just 33.5% of those with ratios between 50% and 59% and just 6.2% of those with ratios above 60%. And even those who are able to be approved with higher debt-to-income ratios likely will pay greater interest rates.

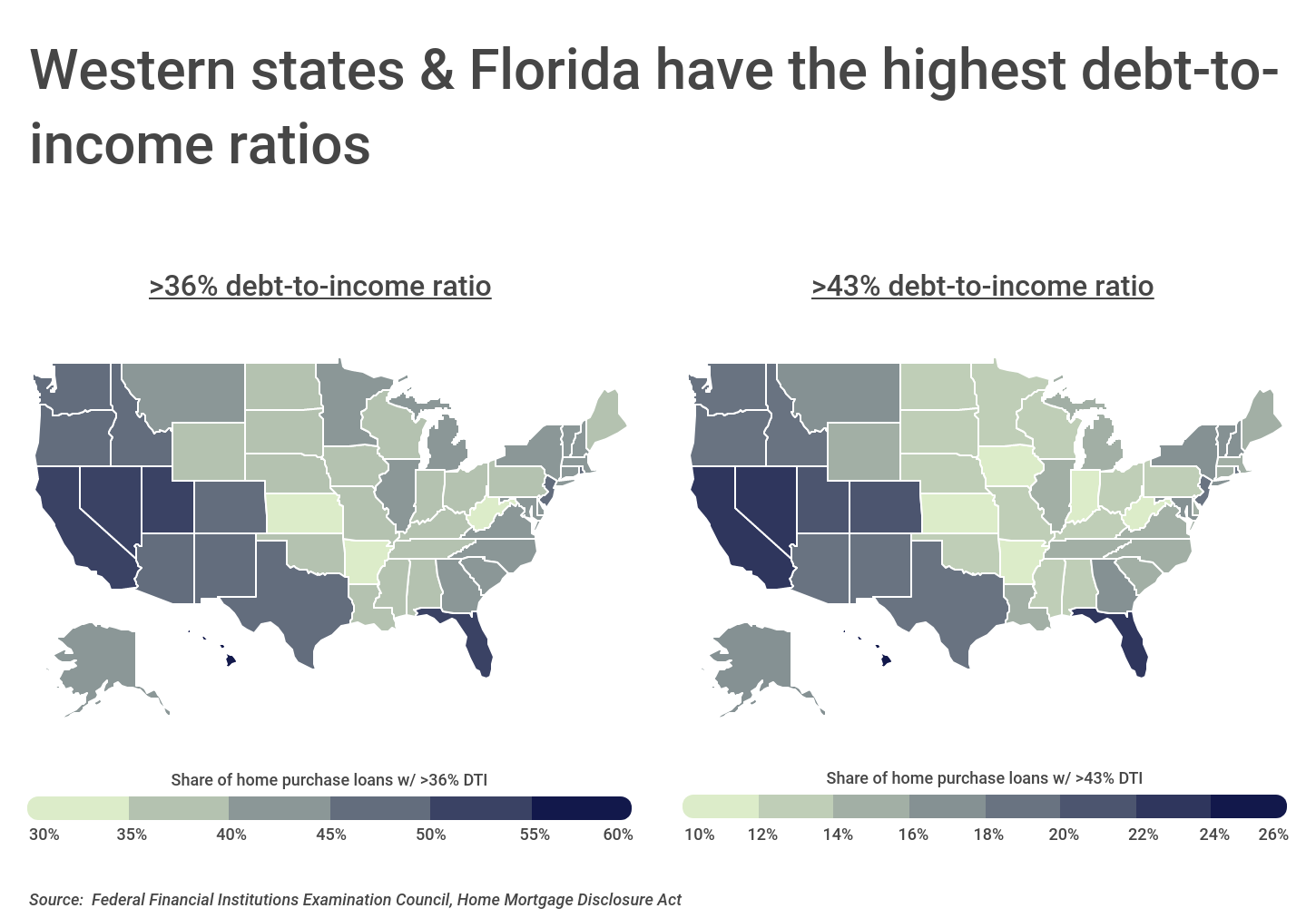

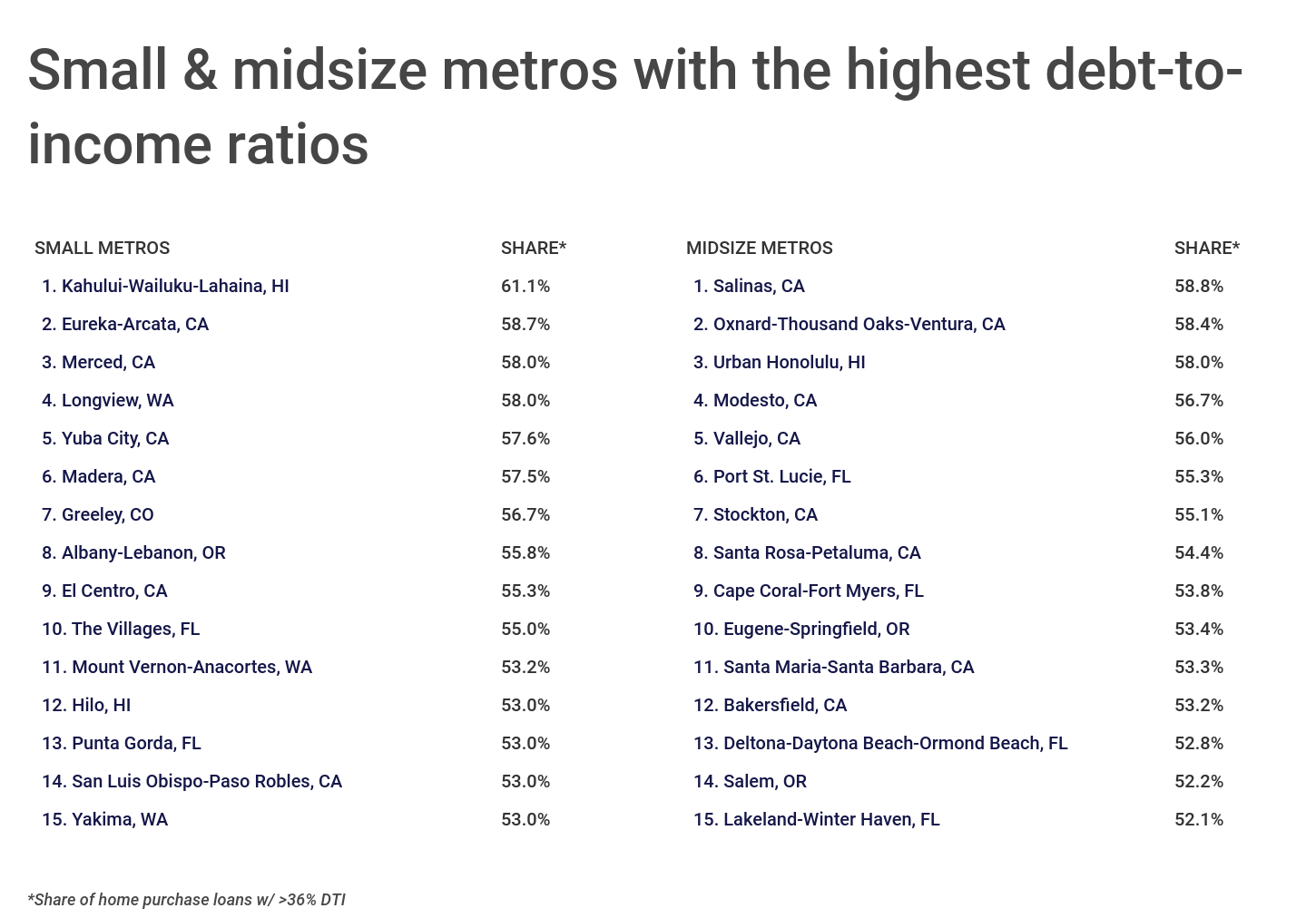

Due to geographic differences in income levels and cost of living, some locations in the U.S. have higher debt-to-income ratios—and more mortgage approvals at higher levels—than other states. States with the most expensive housing, including Hawaii and California, are among the leaders in mortgage approvals at higher debt-to-income ratios because applicants’ existing mortgage payments may be more costly. Most of the other top states with high debt-to-income ratios are also located in the West, with the exception of Florida, which ranks fourth among states for approvals with debt-to-income above 36% and above 43%. And at the local level, the cities with the highest debt-to-income ratios are also most commonly found in states where higher debt-to-income ratios are the norm.

FOR CONSTRUCTION PROFESSIONALS

Software has revolutionized the construction industry. From project management software for construction to takeoff software and estimating software, these new tools improve accuracy, increase efficiency, and reduce costs.

The data used in this analysis is from the Federal Financial Institutions Examination Council’s Home Mortgage Disclosure Act. Only conventional, home purchase loans originated in 2020 were considered. To determine the locations with the highest debt-to-income ratios, researchers at Construction Coverage calculated the share of home purchase loans with a debt-to-income ratio of more than 36%. In the event of a tie, the location with the higher share of home purchase loans with a debt-to-income ratio of more than 43% was ranked higher.

Here are the metropolitan areas with the highest debt-to-income ratios.

Large Metros With the Highest Debt-to-Income Ratios

Photo Credit: ESB Professional / Shutterstock

15. Seattle-Tacoma-Bellevue, WA

- Share of home purchase loans with >36% DTI: 48.9%

- Share of home purchase loans with >43% DTI: 19.2%

- Home purchase loan approval rate for >36% DTI: 89.4%

- Home purchase loan approval rate for >43% DTI: 81.4%

- Home purchase loan approval rate for all loans: 92.1%

- Median interest rate across all home purchase loans: 3.13%

Photo Credit: Gregory E. Clifford / Shutterstock

14. Phoenix-Mesa-Chandler, AZ

- Share of home purchase loans with >36% DTI: 49.3%

- Share of home purchase loans with >43% DTI: 19.7%

- Home purchase loan approval rate for >36% DTI: 89.0%

- Home purchase loan approval rate for >43% DTI: 81.7%

- Home purchase loan approval rate for all loans: 91.3%

- Median interest rate across all home purchase loans: 3.25%

Photo Credit: Travel Bug / Shutterstock

13. San Antonio-New Braunfels, TX

- Share of home purchase loans with >36% DTI: 49.7%

- Share of home purchase loans with >43% DTI: 21.7%

- Home purchase loan approval rate for >36% DTI: 75.6%

- Home purchase loan approval rate for >43% DTI: 62.6%

- Home purchase loan approval rate for all loans: 81.4%

- Median interest rate across all home purchase loans: 3.25%

Photo Credit: Bonnie Fink / Shutterstock

12. Tampa-St. Petersburg-Clearwater, FL

- Share of home purchase loans with >36% DTI: 49.8%

- Share of home purchase loans with >43% DTI: 20.2%

- Home purchase loan approval rate for >36% DTI: 83.3%

- Home purchase loan approval rate for >43% DTI: 72.4%

- Home purchase loan approval rate for all loans: 87.0%

- Median interest rate across all home purchase loans: 3.25%

Photo Credit: thetahoeguy / Shutterstock

11. San Jose-Sunnyvale-Santa Clara, CA

- Share of home purchase loans with >36% DTI: 49.9%

- Share of home purchase loans with >43% DTI: 15.4%

- Home purchase loan approval rate for >36% DTI: 87.8%

- Home purchase loan approval rate for >43% DTI: 75.8%

- Home purchase loan approval rate for all loans: 90.6%

- Median interest rate across all home purchase loans: 2.99%

Photo Credit: Nicholas Courtney / Shutterstock

10. Denver-Aurora-Lakewood, CO

- Share of home purchase loans with >36% DTI: 50.3%

- Share of home purchase loans with >43% DTI: 21.9%

- Home purchase loan approval rate for >36% DTI: 90.3%

- Home purchase loan approval rate for >43% DTI: 83.9%

- Home purchase loan approval rate for all loans: 92.7%

- Median interest rate across all home purchase loans: 3.13%

Photo Credit: Infinity Moments LLC / Shutterstock

9. Orlando-Kissimmee-Sanford, FL

- Share of home purchase loans with >36% DTI: 51.4%

- Share of home purchase loans with >43% DTI: 22.0%

- Home purchase loan approval rate for >36% DTI: 81.2%

- Home purchase loan approval rate for >43% DTI: 70.2%

- Home purchase loan approval rate for all loans: 85.0%

- Median interest rate across all home purchase loans: 3.25%

Photo Credit: Andriy Blokhin / Shutterstock

8. Sacramento-Roseville-Folsom, CA

- Share of home purchase loans with >36% DTI: 51.8%

- Share of home purchase loans with >43% DTI: 20.7%

- Home purchase loan approval rate for >36% DTI: 89.3%

- Home purchase loan approval rate for >43% DTI: 81.6%

- Home purchase loan approval rate for all loans: 91.4%

- Median interest rate across all home purchase loans: 3.13%

Photo Credit: Globe Guide Media Inc / Shutterstock

7. Salt Lake City, UT

- Share of home purchase loans with >36% DTI: 52.4%

- Share of home purchase loans with >43% DTI: 21.8%

- Home purchase loan approval rate for >36% DTI: 89.0%

- Home purchase loan approval rate for >43% DTI: 81.8%

- Home purchase loan approval rate for all loans: 90.8%

- Median interest rate across all home purchase loans: 3.25%

Photo Credit: Gary C. Tognoni / Shutterstock

6. Fresno, CA

- Share of home purchase loans with >36% DTI: 53.3%

- Share of home purchase loans with >43% DTI: 19.9%

- Home purchase loan approval rate for >36% DTI: 89.4%

- Home purchase loan approval rate for >43% DTI: 80.2%

- Home purchase loan approval rate for all loans: 90.1%

- Median interest rate across all home purchase loans: 3.13%

Photo Credit: Sean Pavone / Shutterstock

5. Las Vegas-Henderson-Paradise, NV

- Share of home purchase loans with >36% DTI: 54.9%

- Share of home purchase loans with >43% DTI: 23.4%

- Home purchase loan approval rate for >36% DTI: 85.6%

- Home purchase loan approval rate for >43% DTI: 77.7%

- Home purchase loan approval rate for all loans: 87.8%

- Median interest rate across all home purchase loans: 3.25%

Photo Credit: kan khampanya / Shutterstock

4. San Diego-Chula Vista-Carlsbad, CA

- Share of home purchase loans with >36% DTI: 56.2%

- Share of home purchase loans with >43% DTI: 24.2%

- Home purchase loan approval rate for >36% DTI: 86.9%

- Home purchase loan approval rate for >43% DTI: 78.5%

- Home purchase loan approval rate for all loans: 89.5%

- Median interest rate across all home purchase loans: 3.13%

Photo Credit: Sean Pavone / Shutterstock

3. Los Angeles-Long Beach-Anaheim, CA

- Share of home purchase loans with >36% DTI: 57.9%

- Share of home purchase loans with >43% DTI: 24.8%

- Home purchase loan approval rate for >36% DTI: 86.0%

- Home purchase loan approval rate for >43% DTI: 77.7%

- Home purchase loan approval rate for all loans: 88.7%

- Median interest rate across all home purchase loans: 3.13%

Photo Credit: dorinser / Shutterstock

2. Miami-Fort Lauderdale-Pompano Beach, FL

- Share of home purchase loans with >36% DTI: 58.5%

- Share of home purchase loans with >43% DTI: 26.2%

- Home purchase loan approval rate for >36% DTI: 81.5%

- Home purchase loan approval rate for >43% DTI: 72.9%

- Home purchase loan approval rate for all loans: 83.6%

- Median interest rate across all home purchase loans: 3.25%

Photo Credit: Jon Bilous / Shutterstock

1. Riverside-San Bernardino-Ontario, CA

- Share of home purchase loans with >36% DTI: 60.3%

- Share of home purchase loans with >43% DTI: 26.3%

- Home purchase loan approval rate for >36% DTI: 85.4%

- Home purchase loan approval rate for >43% DTI: 77.3%

- Home purchase loan approval rate for all loans: 87.5%

- Median interest rate across all home purchase loans: 3.13%

Detailed Findings & Methodology

The data used in this analysis is from the Federal Financial Institutions Examination Council’s Home Mortgage Disclosure Act. Only conventional, home purchase loans originated in 2020 were considered. To determine the locations with the highest debt-to-income ratios, researchers calculated the share of home purchase loans with a debt-to-income ratio of more than 36%. In the event of a tie, the location with the higher share of home purchase loans with a debt-to-income ratio of more than 43% was ranked higher. To improve relevance, only metropolitan areas with at least 100,000 residents were included. Additionally, metros were grouped into cohorts based on population size: small (100,000-349,999), midsize (350,000-999,999), and large (1,000,000 or more).