Contractor’s Guide to Choosing a Business Entity

The best business structure for a construction company is typically a Limited Liability Company (LLC) or an S-Corporation, as both shield your personal assets from job site liabilities while providing pass-through tax benefits. However, the right choice for your contracting business ultimately depends on your state’s licensing rules, bonding capacity requirements, and long-term growth plans.

One of the first and most critical decisions that any new business will make when starting out is what type of structure to adopt. Whether you choose a sole proprietorship, LLC, or corporate structure, your decision will have a major impact on your business’s legal risks, tax bills, and growth opportunities. In the construction industry specifically, business structure might even have implications for professional licensing, bonding, and your ability to win jobs.

The right structure for your construction company will depend on factors unique to your business, and there is no one-size-fits-all recommendation. However, it’s worth spending time thinking about the best structure for your circumstances early on: it could mean saving money and avoiding complications later.

Table of Contents

What Is a Business Structure?

Business structure refers to the legal form that a business takes for the purposes of formal recognition by government authorities, paying taxes, and assigning legal liability. The choice of business structure is typically one of the earliest issues a new organization will deal with because government entities like the IRS, state tax agencies, and licensing bodies must know what legal, accounting, and tax requirements to impose on a new entity.

For tax purposes, the Internal Revenue Service classifies businesses into four primary forms: sole proprietorships, partnerships, corporations, and S-corporations. This choice is significant because it determines whether federal tax rates are applied at the entity level, as with C-corporations, or passed through to the individuals involved in the business, as with sole proprietorships, partnerships, and S-corporations.

Depending on the jurisdiction, state law authorizes various business structures. The most common example is the limited liability company (LLC). Like corporations and partnerships, LLCs are established under state law rather than federal law. While the IRS treats LLCs as either disregarded entities, partnerships, or corporations for income tax purposes, it recognizes them as separate entities for employment and certain excise taxes. For income tax, a single-member LLC is treated as a disregarded entity (taxed like a sole proprietorship when owned by an individual), while multi-member LLCs default to partnership status. These classifications depend on the number of members and tax elections typically filed with the IRS following state-level formation. States can also differ in how they regulate LLCs, partnerships, and corporations, resulting in distinct legal considerations and tax requirements for each.

Impacts of Business Structure

Your choice of business structure affects fundamental aspects of the administration and operation of your company. Below are the most important issues to consider:

- Legal liability: Liability determines whether business debts and lawsuits can reach an owner’s personal assets. While formal structures provide a ‘corporate veil’ against general lawsuits, construction owners must be aware that surety companies almost always require personal indemnity for bonding. This means that for your most critical contracts, personal assets may still be at risk regardless of your business structure.

- Taxation: Business structures differ in how profits are taxed. Under the One Big Beautiful Bill Act (OBBBA), the Section 199A deduction for pass-through entities is now permanent, and 100% bonus depreciation has been reinstated, allowing for immediate equipment expensing. For residential contractors, 2025 reforms have also removed the look-back method requirement, significantly simplifying the timing of tax obligations and cash flow management for firms using pass-through structures.

- Ownership and continuity: How ownership is handled determines whether the business can easily add partners, survive the exit of an owner, or transfer to new generations. In construction, continuity is especially relevant for firms that build long-term client relationships or want to bid on multi-year projects, where clients look for stability.

- Formation and compliance requirements: Some structures come into existence automatically, while others require filings and formal documents. For contractors, many states tie professional licensing and public bidding eligibility to formal entities like LLCs or corporations. While bonding eligibility is based on financial strength rather than legal structure, a formal entity is often a prerequisite for the prequalification required to bid on larger public projects.

- Financing and growth: Some structures make it easier to raise money or bring in investors, while others rely heavily on personal financing. Construction businesses often need upfront capital for equipment, payroll, or bonding capacity, so the ability to raise funds isn’t just about expansion—it can determine whether a company can take on larger projects at all.

- Administration: The ongoing obligations of a business structure include taxes, reports, meetings, and fees. More complex structures require more effort to maintain, but they may also offer credibility with clients, lenders, or bonding companies. For a contractor trying to build trust with government agencies or commercial developers, formal structures with higher compliance standards may actually improve competitiveness.

Common Business Structure Types

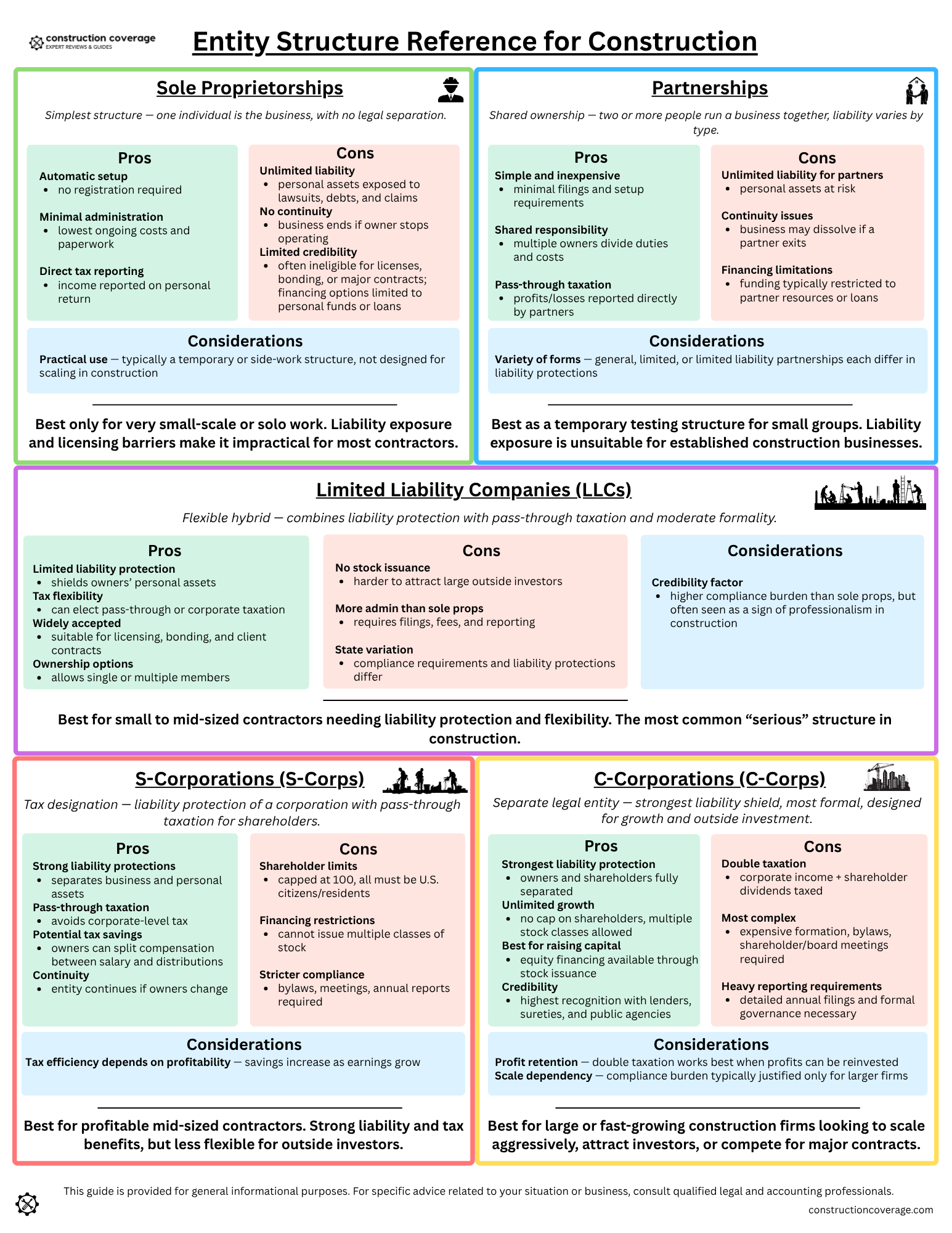

Sole Proprietorship

A sole proprietorship is an unincorporated business that is owned and operated by a single person where no legal distinction exists between the owner and the business. While other structures like LLCs are also unincorporated, a sole proprietorship is the default status for any individual who conducts business activities without registering as a separate legal entity. This structure is simple and requires very limited ongoing administration, but it offers fewer of the advantages that may be available under more complex structures.

Because the individual and the business are effectively one in the same under this structure, the individual operating a sole proprietorship carries unlimited liability, meaning that they are personally responsible for all debts and obligations facing the business. As a “pass-through” entity, all of the business’s profits and losses are reported directly on the sole proprietor’s taxes, and they must pay both income tax and self-employment tax. Sole proprietors also face significant hurdles raising capital because the structure cannot accommodate outside equity investors; any exchange of ownership for funding would require the business to restructure as a partnership or corporation. Additionally, some clients and contractors may prefer the perceived stability and legal separation of a formal entity like an LLC.

Partnership

Partnerships are a relatively simple business structure in which multiple parties share ownership, profits, and losses in a business. The terms of a partnership – including partners’ rights and responsibilities, how decisions about the business will be made, and more – are typically laid out in a legal document called a partnership agreement. While general partnerships require no formal registration, limited partnerships and limited liability partnerships must file formation documents with the state. Aside from these registration requirements and the development of a partnership agreement (which is not required but strongly advised), the ongoing administration of a partnership is relatively inexpensive and straightforward.

From a tax perspective, partnerships are similar to sole proprietorships because profits and losses are passed through to individual partners’ income tax returns. The IRS does require partnerships to report income, losses, and other information each year, but the business does not pay a corporate income tax. This reporting can be somewhat challenging depending on the type and number of partners involved in the business, but it is important for avoiding issues on individual returns.

Liability varies depending on the specific partnership structure. In a general partnership, all partners share unlimited personal liability for the business’s debts and the actions of other partners. In a limited partnership, the business must have at least one general partner carrying unlimited liability, while other partners have limited liability and typically less involvement in management. Finally, in a limited liability partnership, all partners are generally protected from personal liability for the partnership’s debts and the actions of other owners, though they remain personally liable for their own professional negligence or misconduct.

Limited Liability Company (LLC)

Though the IRS does not have a dedicated tax classification for them, limited liability companies (LLCs) are legal entities available in all 50 states and the District of Columbia. LLCs combine liability protections available in corporate structures with the simpler administration and flexibility of partnerships. Depending on the business’s tax elections, the LLC structure may also provide tax advantages.

The laws toward LLCs can vary significantly from state to state. Most importantly, the extent of liability protection offered and states’ treatment of companies for tax purposes can look different across jurisdictions. For example, in some states, single-member LLCs may have weaker ‘charging order’ protections than multi-member LLCs, potentially allowing an owner’s personal creditors to reach business assets. However, the structure still functions as a separate legal entity that shields the owner’s personal property from business-related debts and lawsuits, a critical protection unavailable to sole proprietorships. Business owners may also need to navigate differences across states in formation processes, fees, annual reporting requirements, and other administrative aspects of LLC management, depending on state laws.

Because the IRS does not have a dedicated tax category for LLCs, these entities are taxed by default as either a sole proprietorship (for single-member LLCs) or a partnership (for multi-member LLCs). However, business owners can also elect to be taxed as an S-corporation or C-corporation if those structures offer better tax advantages for their circumstances.

S-Corporation

An S-corporation (S-corp) is less a distinct type of business structure than a particular tax designation for corporations under federal tax law. The S-corp structure includes the pass-through tax advantages of partnerships and sole proprietorships and the strong liability protections available through corporations.

S-corps pass income and losses to owners’ personal tax returns, which means that shareholders pay individual income taxes but not corporate income tax. This allows owners to avoid the “double taxation” that occurs in C-corporations, which can provide significant tax savings.

S-corps, however, come with restrictions and obligations. S-corps are limited to 100 shareholders, and those shareholders must be U.S. citizens or resident aliens. Each shareholder must carefully report their share of the entity’s income, losses, and deductions as part of their personal returns. Administrative requirements are stricter than for LLCs or partnerships, including maintaining bylaws, holding shareholder meetings, and filing annual reports. Failure to comply with these corporate formalities can jeopardize the entity’s liability protection, while violating IRS eligibility rules—such as adding an ineligible shareholder—can lead the corporation to lose its S-corp status and create tax issues for the business.

C-Corporation

A C-corporation (C-corp) is the default type of corporation recognized under federal tax law and most state laws. Like LLCs and S-corporations, C-corps exist as legal entities separate from their owners and shareholders. This structure provides strong liability protection but involves certain disadvantages regarding taxation and more rigid administrative requirements.

One of the main downsides associated with C-corps is taxation. C-corps are distinct entities that must pay tax on their income. The company’s shareholders may receive a distribution of corporate profits, but they also pay personal income tax on these dividends, meaning that corporate profits are effectively taxed twice.

C-corps must adhere to the most formal governance and compliance standards of any structure. This includes creating and maintaining bylaws, issuing stock, holding regular shareholder and board meetings, and filing state annual reports. Additionally, as of 2026, most C-corps must comply with federal Corporate Transparency Act mandates, which include filing detailed beneficial ownership information reports with FinCEN. These requirements add complexity and cost but also create a highly structured framework for running the business.

Despite these drawbacks, C-corps have other advantages, especially for larger or fast-growing firms. C-corps have no limits on the number of shareholders and can easily transfer ownership and sell multiple classes of stock. The C-corp structure is also generally the most appealing for raising capital from investors or pursuing significant expansion.

Construction-Specific Considerations for Choosing a Business Structure

Beyond general tax and liability questions, business structure carries special weight in the construction industry. Contractors face unique regulatory, financial, and reputational requirements that can make certain structures far more practical than others. Key considerations include:

- Licensing: While requirements vary, nearly all states allow individuals and sole proprietorships to hold professional contractor licenses. In some jurisdictions, formalizing as an LLC can actually lead to more complex compliance.

- Bonding & insurance: Surety bonds and specialized insurance policies are often more accessible for formal entities, which insurers may view as more stable. However, requirements vary significantly by state; for instance, California requires LLCs to post an additional $100,000 employee/worker bond that sole proprietors and corporations do not need. Increased bonding capacity is often essential for firms looking to bid on large-scale projects.

- Government and commercial contracts: While large private clients may prefer working with incorporated firms for perceived stability, public agencies typically focus on whether a bidder is a registered legal entity with the necessary bonding capacity and experience. A sole proprietorship that meets these criteria is generally eligible for government contracts, though a formal structure can signal professionalism and long-term commitment.

- Employment and payroll: While all structures can technically hire employees, LLCs and corporations provide clearer frameworks for payroll taxes, workers’ compensation, and compliance with labor laws. These obligations are especially important in construction, where projects may require large crews.

- Perception and credibility: Prospective clients, investors, subcontractors, and vendors may feel more confident working with a business that has a formal structure such as an LLC, S-corp, or C-corp, rather than a sole proprietorship. A formal entity can signal stability, professionalism, and long-term commitment.

The Most Common Business Structures in the Construction Industry

Because of the variety of business structures and the unique circumstances for every company, it is hard to say which structure will be right for your construction business. However, certain structures tend to be more common in some situations for the construction industry.

Sole proprietorships and partnerships are a potential option for very small contractors who prefer relatively simple administration or those just starting out and testing the viability of a new business. However, as your business grows and the risks and complexities you face increase, it may be appropriate to transition to a different form. In particular, the liability risks associated with work in construction and building trades may make sole proprietorship and partnership structures less desirable.

LLCs are a good option for many small to mid-sized construction companies. They provide liability protection, allow for single members or multiple owners, and are flexible enough to allow for the business to grow. However, it is important to note that LLCs are not a recognized structure for federal tax purposes. By default, the IRS treats single-member LLCs as sole proprietorships and multi-member LLCs as partnerships, though you can also choose to make a tax election to be treated as a corporation.

S-corporations are also a popular option with small to mid-sized contractors, especially those that are poised to grow. In addition to limited liability protection, the primary benefit of S-corps is that they allow pass-through taxation. Owners in an S-corp can accept a reasonable salary and receive the remaining profit as a distribution, which is not subject to self-employment taxes. Because S-corps are pass-through entities, these profits are only taxed at the individual level, allowing the business to avoid the double taxation of a corporate income tax. If the business is growing and profitable, this setup can result in considerable tax savings for the owner.

Finally, C-corporations will tend to be most appropriate for large builders. The more extensive administrative requirements and higher associated costs are best handled in more established firms with legal and financial expertise available. While the corporate structure has benefits in the form of very strong liability protections and the ease of transferring ownership and raising capital, these advantages are less relevant for smaller companies.

Download the Entity Structure Reference Sheet for Construction PDF

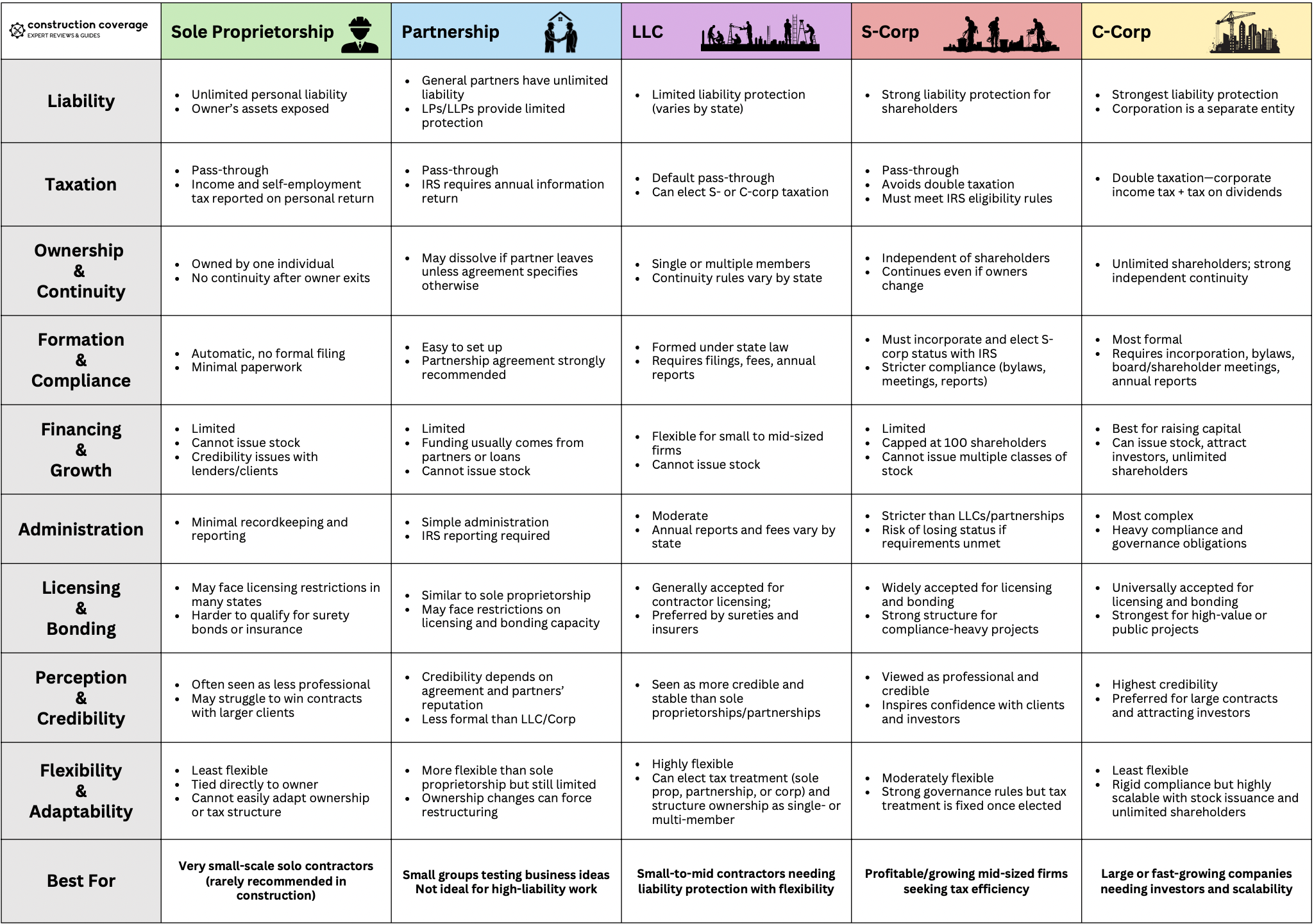

Entity Structure Comparison Table for Construction Businesses

| Sole Proprietorship | Partnership | LLC | S-Corp | C-Corp | |

|---|---|---|---|---|---|

| Liability | Unlimited personal liability; owner’s assets exposed | General partners have unlimited liability; LPs/LLPs provide limited protection | Limited liability protection (varies by state) | Strong liability protection for shareholders | Strongest liability protection; the corporation is a separate entity |

| Taxation | Pass-through; income and self-employment tax reported on personal return | Pass-through; IRS requires an annual information return | Default pass-through; can elect S- or C-corp taxation | Pass-through; avoids double taxation; must meet IRS eligibility rules | Double taxation—corporate income tax + tax on dividends |

| Ownership & Continuity | Owned by one individual; no continuity after owner exits | May dissolve if partner leaves unless agreement specifies otherwise | Single or multiple members; continuity rules vary by state | Independent of shareholders; continues even if owners change | Unlimited shareholders; strong independent continuity |

| Formation & Compliance | Automatic, no formal filing; minimal paperwork | Easy to set up; partnership agreement strongly recommended | Requires filing Articles of Organization with the state; ongoing compliance includes annual reports and maintaining a registered agent | Must incorporate and elect S-corp status with IRS; stricter compliance (bylaws, meetings, reports) | Most formal; requires incorporation, bylaws, board/shareholder meetings, and annual reports |

| Financing & Growth | Limited; cannot issue stock; credibility issues with lenders/clients | Limited; funding usually comes from partners or loans; cannot issue stock | Flexible for small to mid-sized firms; cannot issue stock | Limited; capped at 100 shareholders; cannot issue multiple classes of stock | Best for raising capital; can issue stock, attract investors, unlimited shareholders |

| Administration | Minimal recordkeeping and reporting | Simple administration; IRS reporting required | Moderate; annual reports and fees vary by state | Stricter than LLCs/partnerships; risk of losing status if requirements are unmet | Most complex; heavy compliance and governance obligations |

| Licensing & Bonding | May face licensing restrictions in many states; harder to qualify for surety bonds or insurance | Similar to sole proprietorship; may face restrictions on licensing and bonding capacity | Generally accepted for contractor licensing; preferred by sureties and insurers | Widely accepted for licensing and bonding; strong structure for compliance-heavy projects | Universally accepted for licensing and bonding; strongest for high-value or public projects |

| Perception & Credibility | Often seen as less professional; may struggle to win contracts with larger clients | Credibility depends on agreement and partners’ reputation; less formal than LLC/Corp | Seen as more credible and stable than sole proprietorships/partnerships | Viewed as professional and credible; inspires confidence with clients and investors | Highest credibility; preferred for large contracts and attracting investors |

| Flexibility & Adaptability | Least flexible; tied directly to owner; cannot easily adapt ownership or tax structure | More flexible than sole proprietorship but still limited; ownership changes can force restructuring | Highly flexible; can elect tax treatment (sole prop, partnership, or corp) and structure ownership as single- or multi-member | Moderately flexible; strong governance rules but tax treatment is fixed once elected | Least flexible; rigid compliance but highly scalable with stock issuance and unlimited shareholders |

| Best For | Very small-scale solo contractors (rarely recommended in construction) | Small groups testing business ideas Not ideal for high-liability work | Small-to-mid contractors needing liability protection with flexibility | Profitable/growing mid-sized firms seeking tax efficiency | Large or fast-growing companies needing investors and scalability |

Download a PDF version of this table—Entity Structure Comparison Table for Construction Businesses

Download the Entity Structure Comparison Table for Construction Companies PDF

Additional Resources for Choosing Your Business Structure

Because the choice of business structure is such a consequential decision and may be unique to your own circumstances, it is important to consult with qualified professionals and reliable sources of information when choosing what structure to take. Below are some resources to consider:

- Accountants and Tax Professionals: A skilled accountant can offer expert advice on how a business structure will impact your potential tax burden, both as an individual and for the business.

- Attorneys: Experts in small business law will be able to help you understand considerations for taxes and liability in your state and help you navigate the process of filing to form or organize your business entity. If you are aiming to transition your business structure, you may need a lawyer to handle changes in ownership/membership and drafting relevant legal documents such as operating agreements or bylaws.

- Government Authorities: The IRS, the U.S. Small Business Administration, the Secretary of State’s office in the state where you form or operate, and the Financial Crimes Enforcement Network (FinCEN) are excellent sources of information about the different options and federal reporting requirements for your business’s structure. The SBA co-funds a national network of Small Business Development Centers in partnership with state and local organizations to provide technical assistance on these types of questions to new and small businesses. State licensing or regulatory bodies may also be able to provide industry-specific insights about business structure requirements unique to businesses in construction and building trades.

- Insurance and Bonding Agents: Because construction firms often require insurance or bonding capacity in order to maintain licensure and win bids, it may be worth consulting an insurance agent or surety bond producer to understand the potential impacts of your choice of business structure.