Understanding Labor Burden

Labor burden is the added expense a company pays on top of employee wages to cover benefits, taxes, and other employment-related costs.

Labor burden refers to the total cost a business incurs to employ someone beyond their base wages or salary. These indirect expenses—including taxes, insurance, benefits, and PTO—are added to base wages to determine an employee’s ‘fully burdened labor rate.’

This comprehensive figure accounts for payroll taxes, workers’ compensation insurance, and other job-specific expenses like safety training or personal protective equipment. While this concept applies across all industries, it plays a particularly important role in construction, where indirect costs tied to each worker can be substantial and often vary by project type, location, or trade.

In construction accounting, labor burden is used to understand the full financial impact of labor on a project and to ensure that estimates, bids, and budgets account for more than just hourly wages. It helps contractors track and recover all labor-related costs and avoid underpricing work due to hidden or overlooked expenses. Understanding labor burden allows for more accurate job costing, better financial planning, and healthier project margins.

Table of Contents

Why Labor Burden Is Important in Construction

In construction, labor is one of the largest and most variable project expenses. While base wages are easy to quantify, they represent only part of the actual cost of employing a worker. Payroll taxes, insurance premiums, paid leave, and training add significantly to labor-related spending—but are often less visible during estimating. Labor burden captures these costs and brings them into the open, allowing contractors to budget for them accurately. Because these costs are highly volatile (e.g. insurance premiums up 10–20% in 2026), experts recommend recalculating labor burden at least twice per year.

Without accounting for labor burden, job costs are understated, bids may come in too low, and profit margins can erode over time. Accurate labor burden calculations support reliable estimates, help avoid underpricing, and provide a clearer view of project performance. In competitive markets where small differences in cost can determine whether a bid is won or lost, a well-understood labor burden can make the difference between a profitable project and a financial loss.

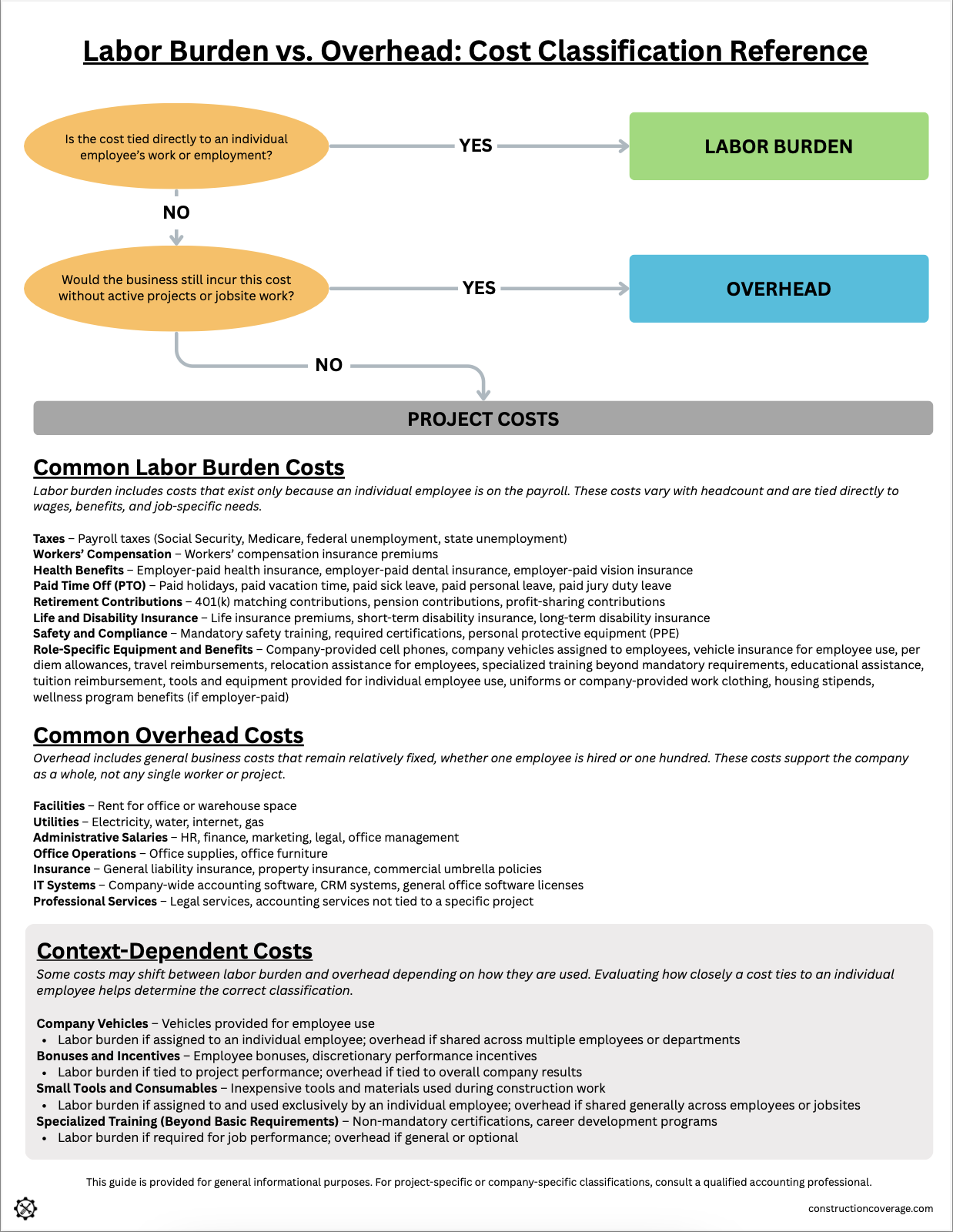

What Costs Are Included in Labor Burden?

Labor burden includes any cost directly tied to employing a specific worker—costs that arise when someone joins the payroll and disappear when they leave. While burdened costs vary by company, trade, job role, union agreements, and location, most labor burden calculations include several common categories:

- Payroll Taxes — The employer’s share of Social Security and Medicare taxes (FICA), federal unemployment (FUTA) taxes, and state unemployment (SUTA) taxes. In many jurisdictions, this also includes mandatory contributions for State Paid Family and Medical Leave (PFML) and State Disability Insurance (SDI). These taxes are required by law and apply to nearly all employees.

- Workers’ Compensation Insurance — Premiums paid to insure employees for job-related injuries or illnesses. Rates vary significantly based on job classification codes, risk levels, and state regulations. Learn more and compare workers’ compensation policies in this guide.

- Health Benefits — Employer-paid health, dental, and vision insurance premiums. In union environments, these benefits may also include contributions to multiemployer health plans.

- Paid Time Off (PTO) — Costs associated with paid holidays, vacation time, sick leave, personal days, and jury duty leave. Even when employees are not working, businesses continue to incur payroll and benefit expenses.

- Retirement Contributions — Employer contributions to employee retirement plans, such as 401(k) matching, profit-sharing, or pension fund payments. While some contributions are discretionary, many employers are now subject to mandatory automatic enrollment requirements.

- Life and Disability Insurance — Employer-paid premiums for life insurance, short-term disability insurance, and long-term disability insurance.

- Safety and Compliance Costs — Mandatory safety training, certifications, and personal protective equipment (PPE) issued to employees to meet jobsite and regulatory requirements.

- Role-Specific Equipment and Benefits — Costs associated with job-specific tools and perks. Examples include company-provided cell phones, per diem allowances, travel reimbursements, relocation assistance, educational assistance or tuition reimbursement, specialized training beyond basic requirements, employee-use tools and equipment, uniforms or work clothing, housing stipends, and employer-paid wellness benefits. Note that while company vehicles are a significant expense, they are typically categorized as equipment overhead rather than labor burden because ownership and insurance costs remain even if the employee leaves the company.

Contractors must account for each of these costs to accurately measure the true cost of employing workers.

Labor Burden vs. Overhead

Labor burden and overhead both represent costs that are not immediately visible in an employee’s base wages or a project’s direct materials. However, they serve different purposes in construction accounting and should be tracked separately. Labor burden includes costs tied directly to employing a worker, such as payroll taxes, workers’ compensation insurance, paid time off, and role-specific expenses like safety training or personal protective equipment. These costs fluctuate with staffing and are specific to individual employees.

Overhead, by contrast, covers the general costs of running the business that are not linked to a specific employee’s labor. While expenses like office rent and certain utilities may remain relatively stable, others—such as general liability insurance, administrative salaries, and company-wide software—often scale as a company grows. For example, general liability premiums are typically auditable and will increase alongside a contractor’s total payroll or revenue.

Accurately separating labor burden from overhead supports better job costing, more reliable bidding, and clearer financial reporting. Misclassifying these costs can lead to underpricing, margin erosion, and project tracking errors.

For a quick reference to easily distinguish between labor burden and overhead costs, download our cost classification reference guide below.

Download the Labor Burden vs. Overhead Cheatsheet

How to Calculate Labor Burden

Labor burden measures the true cost of employing a worker beyond their base wages or salary. For business owners and contractors, it answers a critical question: how much does each employee really cost the company?

There are several ways to express the costs of employing a worker depending on what a business wants to evaluate:

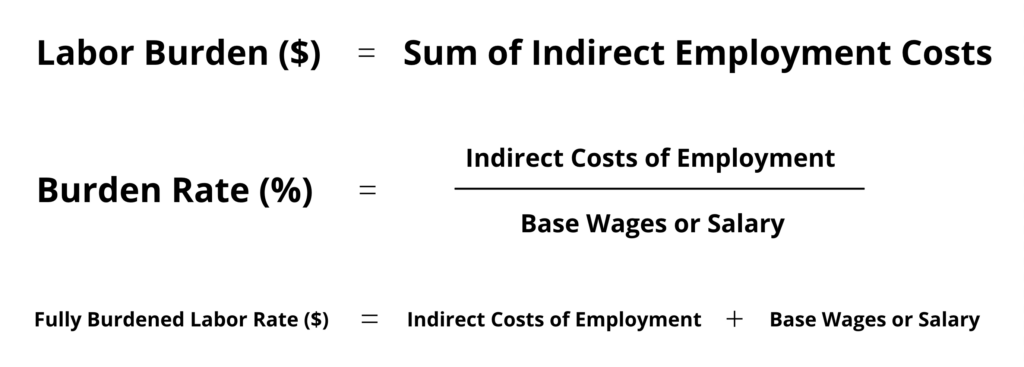

Labor Burden ($) is the total dollar amount of indirect employment costs. This figure is useful when budgeting for specific fringe benefits and payroll taxes, or when reviewing the financial impact of staffing and benefit decisions.

Burden Rate (%) is the percentage of indirect costs relative to base wages. This metric is helpful for tracking cost trends over time, comparing the overhead requirements of different departments or roles, and spotting major shifts in labor-related expenses.

Fully Burdened Labor Rate ($) is the combined cost of base wages plus all burden costs, shown as an hourly or annual figure. Essential for setting accurate billing rates, calculating break-even costs, and managing project cash flow.

Each measure offers a different lens on labor costs. Contractors may focus on the fully burdened labor rate when pricing work to ensure all expenses are captured, while businesses managing crews or departments may rely more on burden rates to monitor the company’s overhead load and control indirect labor costs. Knowing how to calculate and apply all three gives companies stronger control over job costing, estimating, and financial planning.

Example Calculations

To see these equations in action, consider a simple example for a construction superintendent. Here are the details:

Base Wages: $80,000 per year

Indirect Employment Costs:

- Payroll taxes (Social Security and Medicare): $6,120

- Workers’ compensation insurance: $3,200

- Employer-paid health, dental, and vision insurance: $8,500

- Paid time off: $4,000

- Retirement contributions (401k match): $2,400

- Safety training and equipment: $800

Calculations

Labor Burden ($) = $6,120 + $3,200 + $8,500 + $4,000 + $2,400 + $800 = $25,020 per year

Burden Rate (%) = $25,020 ÷ $80,000 = 31.3%

Fully Burdened Labor Rate = $80,000 + $25,020 = $105,020 per year = $50.49 per hour

Average Labor Burden Rates

While the cost to employ people varies widely by industry, company size, and workforce structure, the U.S. Bureau of Labor Statistics publishes detailed compensation data that offers a useful benchmark. By annualizing the figures from the BLS December 2025 Employer Costs for Employee Compensation (ECEC) report, business owners can better understand labor burden across the private sector and within the construction industry.

Annual

Hourly

Annualized data from the BLS report shows that across all private industry full-time workers, an employer will pay $110,240 per year in total compensation. Of that, $75,629 is direct wages or salary, and $34,611—or roughly 46% of base pay—is spent on benefits and legally required costs. The costs of employment (i.e. labor burden) break down as follows:

- Paid leave – $9,069 (12.0% of wages)

- Supplemental pay – $4,846 (6.4%)

- Insurance benefits – $9,048 (12.0%) *

- Retirement and savings – $3,994 (5.3%)

- Legally required benefits – $7,654 (10.1%)

In the construction industry, based on the BLS data, a full-time construction employee costs $107,474 in total compensation, with $74,630 in wages and $32,843 in labor burden costs. The labor burden amounts to approximately 44% of base pay. Here’s how that burden breaks down:

- Paid leave – $5,491 (7.4% of wages)

- Supplemental pay – $5,366 (7.2%)

- Insurance benefits – $7,966 (10.7%) *

- Retirement and savings – $4,950 (6.6%)

- Legally required benefits – $9,069 (12.2%)

These benchmarks highlight just how expensive labor burden can be for businesses—exceeding 45% of base wages on average for all private industry workers. While every construction business will have its own structure, benefits, and insurance costs, comparing actual burden rates to national averages can help contractors refine their budgets, bids, and job costing strategies to remain competitive.

* According to the 2025 KFF Employer Health Benefits Survey, the average employer contribution to premiums was approximately $7,885 for single coverage and $20,143 for family coverage.

Tracking Labor Costs

Tracking labor burden manually—especially across multiple projects, roles, and time periods—can be complex and error-prone. Most contractors rely on construction accounting software or job costing tools to manage burden rates, report them consistently, and monitor changes over time. These platforms allow businesses to compute burden rates at the employee, crew, or job level—and apply the appropriate cost codes to ensure accurate job costing and financial reporting.

When paired with estimating software, accurate labor burden rates can be applied during the bidding phase to ensure true labor costs are reflected in proposals. Likewise, project management software with time tracking and job costing capabilities can help contractors see how the costs of employment affects ongoing budgets and project profitability.

By combining the right software with accurate inputs, contractors can track labor burden more effectively, reduce risk of underbidding, and improve confidence in their cost estimates.

Frequently Asked Questions

What is the difference between a base wage and a fully burdened labor rate?

The base wage is the gross hourly pay an employee earns before taxes or deductions. The fully burdened labor rate is the base wage plus all indirect costs the employer pays to keep that worker employed, such as payroll taxes, insurance, and benefits.

Is labor burden the same as overhead?

No, labor burden is not the same as overhead. Labor burden only includes the indirect costs directly associated with employing your field workforce (taxes, benefits, insurance). Overhead refers to the general administrative costs of running your business that cannot be tied to a specific project or worker, such as office rent, executive salaries, software subscriptions, and marketing.

How do you calculate labor burden in construction?

To calculate labor burden, total all indirect employer costs (taxes, insurance, benefits, allowances) for a specific period. Divide that total by the total direct payroll (base wages) for the same period, then multiply by 100 to get your labor burden percentage. Apply this percentage to an employee’s base hourly wage to find their true hourly cost.

Are workers’ compensation premiums included in the labor burden?

Yes. Workers’ compensation is a mandatory employer expense tied directly to your payroll and trade risk, making it a core component of your labor burden. In construction, workers’ comp premiums are often the largest single burden expense after standard payroll taxes.

What is a good labor burden rate?

There is no universal “good” rate, as it depends heavily on your location, union requirements, and trade risk class. However, a typical construction labor burden ranges from 30% to 60% of the base wage. High-risk specialty trades, like roofing, will naturally have higher rates due to elevated workers’ compensation premiums.

References

- BLS Employer Costs for Employee Compensation Survey. A national BLS survey that measures the average hourly cost of wages, salaries, and specific employee benefits.

- KFF Employer Health Benefits Survey. A national survey that tracks annual trends in employer-sponsored health coverage, including premium costs and employee contributions.

Related Posts

The Best Construction Accounting Software for 2026

The best construction accounting software of 2026 is CMiC (Best Overall), followed closely by FOUNDATION (Runner-Up) and QuickBooks (Best for…

How to Track Construction Costs Using Standardized Cost Codes

Tracking construction costs requires categorizing every labor, material, and equipment expense using a standardized list of cost codes. This provides…

What is Retainage in Construction?

Retainage is the portion of a contract price (typically 5% to 10%) intentionally withheld from progress payments until a project…

What Is Job Costing in Construction Accounting?

Job costing is an accounting method that enables contractors and construction companies to track, budget, and manage the costs associated…

Guide to Understanding Construction Accounting

Introduction to Construction Accounting Successful construction companies use a different accounting approach than other businesses. In many industries, companies focus…

Construction Cost Codes: Standard List & Free PDF Download

A construction cost code is a standardized numerical identifier used to categorize and track specific labor, material, and equipment expenses.…

QuickBooks for Contractors: 2026 Editions & Feature Comparison

Choosing the right QuickBooks edition for your construction business in 2026 comes down to matching your company's size and daily…