General Liability vs. Professional Liability Insurance in Construction

While general liability covers physical "occurrences" (accidents) and professional liability covers "wrongful acts" (errors), the distinction between the two has blurred. Modern endorsements can pull professional-driven property damage back into the CGL policy, while combined contractors professional liability (CPrL) forms now bundle design, workmanship, and repair cost coverage.

Key Takeaways

- Core Differences: Contractor general liability (CGL) covers physical jobsite accidents (like bodily injury or third-party property damage), while professional liability (CPrL) covers financial or physical harm caused by errors in professional judgment, such as design flaws or scheduling mistakes.

- Coverage Gaps: Standard CGL policies exclude “professional services” and generally will not pay to fix your own faulty physical workmanship. The modern CPrL bundle is specifically designed to step in and fill both of these gaps.

- Tech and Delivery Risks: As design-build models expand and contractors increasingly rely on AI-assisted tools and 3D modeling (BIM), standard CGL policies are actively excluding these modern tech exposures, making a dedicated professional liability policy essential.

- Proactive Protection: Modern CPrL policies often include contractors errors and omissions and rectification coverages. These can actually pay you directly to fix a physical mistake or design error before a formal third-party lawsuit is ever filed.

Contractor general liability insurance primarily covers physical accidents, such as third-party bodily injury and property damage, that happen during active operations on the jobsite. It can also respond to certain claims that show up after the project is complete, but it will never cover pure economic loss. Contractors professional liability insurance, by contrast, covers financial losses, physical damages, and bodily injury tied to professional errors, like negligent advice, design flaws, or project management mistakes.

While these policies used to sit in separate silos, modern endorsements and combined policy forms can blur the lines between a site accident and a professional error. Most contractors end up needing both because standard CGL policies include a strict “professional services” exclusion. If a structural collapse traces back to a flawed blueprint or a value-engineering decision instead of poor physical workmanship, the CGL carrier may deny the claim.

Even if you add a give-back endorsement like CG 22 80 to your CGL policy to restore coverage for physical damage caused by your design, that endorsement still will not pay for project delays or the cost to tear out and fix the mistake. To get that level of protection, contractors rely on the modern CPrL bundle, which often includes contractors errors and omissions for faulty physical workmanship and rectification coverage to fund proactive repairs.

That split matters more than it used to. In 2026, many contractors rely on AI-assisted estimating, 3D modeling (BIM), and automated site planning to tighten bids and solve coordination problems. The catch is that once you are modeling, coordinating, or recommending design alternatives, you may be performing “professional services” in the legal sense. Insurers have also started drawing clearer lines around new tech: standard CGL policies increasingly include newer ISO endorsements (such as CG 40 47) that can restrict or exclude claims tied to generative AI.

If you are not clear on where your CGL stops and your contractor professional liability begins, you can get forced into paying a claim out of pocket. As design-build and construction manager at risk (CMAR) continue to expand, owners are also tightening insurance requirements and asking for dedicated professional liability policies to close gaps that CGL will not touch.

Terminology Warning

In the construction industry, project owners, lenders, and even insurance brokers frequently use the terms “professional liability” and “errors and omissions” (E&O) interchangeably. While these terms mean the exact same thing in other professions, construction underwriters treat them as distinct coverages:

- Professional Liability: Covers mistakes in professional services—such as design, engineering, scheduling, or project management—that result in third-party financial loss, physical property damage, or bodily injury.

- Contractors Errors and Omissions: Covers the physical cost to repair or replace your own faulty physical workmanship (often referred to as property damage to your work). This fills the exact gap left by the workmanship exclusions in a standard general liability policy, and it can often be structured to pay you directly to fix the physical error before a claim is filed.

- Rectification and Mitigation: A proactive, first-party coverage that pays the direct costs to repair or replace bad work caused by your firm’s professional design or engineering errors. However, the mistake must be discovered before it leads to a formal third-party lawsuit.

The remainder of this guide explores both core professional liability and the modern combined bundle, showing exactly how these coverages differ from (and fill the gaps left by) a standard general liability policy.

Related Guides on GL & PL

Table of Contents

- What Are the Core Differences Between CGL and CPrL?

- What Is Contractor General Liability (CGL) Insurance?

- What Is Professional Liability Insurance for Contractors?

- Why Design-Build Firms & Construction Managers Need Both

- GL vs. PL: Real-World Construction Scenarios

- Cost Comparisons & Factors for Contractors

- Securing Your Business & Closing the Gaps

- Frequently Asked Questions about General Liability & Professional Liability

- How are legal defense costs handled differently between General and Professional Liability?

- Will professional liability insurance cover a bidding or estimating error?

- Do artisan subcontractors (like plumbers or electricians) need professional liability insurance?

- What is a "Retroactive Date" and why does it matter when switching policies?

- Can I buy professional liability insurance for just one specific construction project?

- References & Additional Resources

- Related Posts

What Are the Core Differences Between CGL and CPrL?

The cleanest way to separate these policies is to look at the cause of loss, policy trigger, and exclusions.

Cause of Loss

General liability responds when your operations cause an accident or harmful condition. A modern contractors professional liability bundle, however, responds on multiple fronts. The core professional coverage responds when an error in your judgment—such as design, coordination, or management—causes harm. Meanwhile, the contractors errors and omissions portion applies when your faulty physical workmanship causes a financial loss, and the rectification piece triggers the moment you discover a design error that needs an immediate fix.

Policy Trigger

Timing is another key difference. General liability is typically written on an occurrence basis, meaning it covers damage that happens during the policy year, even if the claim gets filed later. Professional liability is often written on a claims-made basis, meaning it’s triggered when a claim or demand is made against you (and subject to retro dates and reporting requirements); occurrence-based professional policies are far less common for contractors and usually only available via specific endorsements.

Exclusions

Where contractors get burned is the exclusion language. Standard general liability policies for contractors typically exclude professional services by endorsement. So if a physical collapse traces back to value engineering, BIM coordination, delegated design oversight, or a spec decision, the GL carrier may deny the claim.

CGL policies also contain a “your work” exclusion, meaning they generally will not pay to repair or replace your own self-performed faulty construction (though an exception typically applies to work done by subcontractors). That is why a dedicated contractors professional liability bundle matters: it closes both gaps. It covers pure economic loss, bodily injury, and property damage resulting from professional mistakes, while also providing a financial safety net to fix your own faulty workmanship.

CGL vs. CPrL Detailed Comparison

| The CPrL Bundle | ||||

| Feature | General Liability | Professional Liability | Contractors Errors & Omissions | Rectification & Mitigation |

| Primary Cause of Loss | Physical accident or occurrence | Negligent act or error in design, coordination, or management | Faulty physical workmanship | Discovered design or engineering error |

| Policy Trigger | Occurrence (when the damage happens) | Claims-made (when a third party sues or demands money) | Claims-made (when a third party demands money for bad work) | First-party discovery (when you find the mistake before a claim) |

| Type of Harm Covered | Third-party bodily injury or tangible property damage | Third-party pure economic loss, bodily injury, or property damage | Direct first-party costs to correct a physical workmanship mistake | Direct first-party costs to correct a professional error/design defect |

| Core Focus | Means, methods, and site safety | Design, advice, coordination, and project management | Physical installation and trade work | Proactive problem solving and preventing lawsuits |

| Key Exclusions | Professional services and damage to your own work | Faulty physical workmanship | Professional design services | Errors discovered after a formal third-party claim is already made |

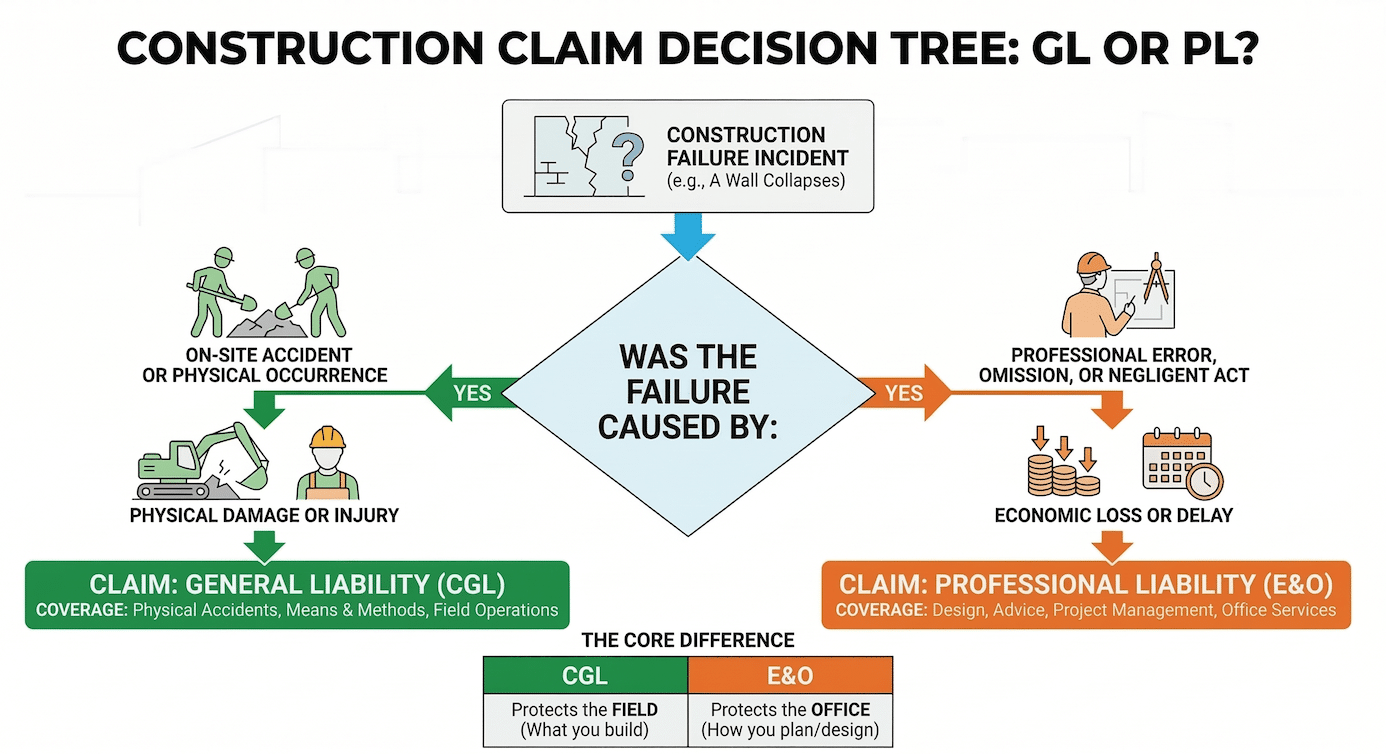

Claim Flowchart: GL or PL?

A visual decision tree to help contractors determine if General Liability or Professional Liability will respond to a specific construction failure.

START: A Construction Failure Occurs

(e.g., Wall collapses, water leak, massive project delay)

STEP 1: Does the claim involve physical property damage or third-party bodily injury?

NO (Something other than physical property damage or bodily injury)

Pure financial/economic loss ONLY (e.g., project delay, lost rent, extended financing)

Professional Liability (PL)

Standard CGL explicitly excludes pure economic loss without tangible physical damage.

A design or engineering error discovered BEFORE it causes a failure or lawsuit

Rectification & Mitigation (CPrL)

A first-party endorsement that pays you directly to fix the mistake proactively.

YES (Physical property damage or injury has occurred)

STEP 2: What was the root cause of the physical damage or injury?

An error in professional judgment, design, BIM coordination, or value engineering

Professional Liability (PL)

Standard CGL denies coverage for physical failures tied to design via the “Professional Services” exclusion.*

A physical jobsite accident or a physical labor mistake

STEP 3: Is the claim strictly for the cost to tear out and fix your own faulty physical workmanship?

YES (e.g., A crew simply built a wall out of plumb, requiring a tear-down)

Contractors Errors & Omissions

CGL denies this via the “Your Work” exclusion. You need this specific CPrL bundle endorsement to cover physical labor fixes.**

NO (The site accident caused resulting damage to third-party property or injured someone)

General Liability (CGL)

CGL is triggered by an occurrence, covering active site accidents (Premises-Operations) or completed operations.

*Note: If you have a CG 22 80 endorsement on your CGL, it may restore coverage for bodily injury or resulting physical damage caused by your own design work, but it still will not cover project delays or the cost to fix the mistake itself.

**Note: Under a standard CGL policy, the “Your Work” exclusion contains a Subcontractor Exception. If the faulty physical workmanship was performed by a subcontractor rather than your own employees, CGL may cover the damage to that work, provided your policy does not include an endorsement (such as CG 22 94) that removes this exception.

What Is Contractor General Liability (CGL) Insurance?

General liability insurance protects a business against claims of third-party bodily injury, property damage, and personal or advertising injury arising from day-to-day operations. It’s the baseline layer of liability protection for most contractors, and GL is commonly required by project owners, lenders, and state licensing boards.

Coverage & Policy Triggers

Standard general liability coverage is built around two primary triggers. The first is an occurrence, defined not only as a sudden accident but also as the “continuous or repeated exposure to substantially the same general harmful conditions” (for example, a slow hidden water leak that causes rot over time). The second is an offense, which protects against certain intangible harms such as libel, slander, or copyright infringement in your advertising.

In practice, the physical protection is split into two buckets:

- Premises-Operations: Handles liability while you are on-site and the work is in progress. If a framing crew fails to brace a wall properly and it collapses onto a neighboring structure, the neighbor’s property damage and related injuries generally fall under this active operations bucket.

- Products-Completed Operations (PCO): Once the project is finished and turned over, PCO takes over. This covers the “long tail” of risk, such as a weld failing on a balcony handrail two years after completion and injuring a tenant.

For many contractors, the biggest value in CGL is the duty to defend. Even meritless allegations can trigger expensive defense costs. Attorneys’ fees, expert witness fees, and court costs in a serious construction defect case can easily reach six figures. A general liability policy puts the carrier on the hook for the legal response for both active site accidents and completed operations claims, so a single slip-and-fall or post-completion defect doesn’t drain cash reserves.

Key Exclusions

Even with broad protection, general liability is not a warranty for workmanship. The policy includes a “your work” exclusion. If your in-house crew installs a defective pipe that later leaks and ruins the new hardwood floors you also installed, the carrier will typically deny the entire claim. They will not pay to fix the pipe, nor will they pay to replace the ruined floor, because the entire project is considered your work.

However, if the defective work was performed on your behalf by a hired subcontractor, the “your work” exclusion typically does not apply. For example, if a subcontracted plumber installs that same defective pipe and it ruins the floor, the general liability policy will generally cover the cost of the ruined floor but not the replacement of the defective pipe itself. Because the standard policy contains an express exception for work performed by subcontractors, it restores coverage for resulting damage to the project that would otherwise be excluded if performed by your in-house crew, though the cost to fix the specific faulty workmanship remains an uncovered business risk.

Additionally, standard general liability policies contain a strict “professional services” exclusion. If property damage is caused by a design error or a technical calculation rather than a physical construction mishap, the carrier will likely deny the claim. To a general liability carrier, installing a wall is a covered operation, but deciding where a load-bearing wall needs to be placed is an uncovered professional service.

Common Endorsements

To tailor a standard policy to actual construction risks and bridge the gaps in standard coverage, contractors frequently add specific endorsements:

- Limited Exclusion – Contractors – Professional Liability (CG 22 80): This is a critical “give-back” endorsement for design-build contractors. It restores general liability coverage for professional errors, but only if those errors occur in connection with construction work you are also performing. It ensures that if your design causes a physical collapse during or after the build, your policy still responds to the resulting damages.

- Additional Insured Endorsements (CG 20 10 and CG 20 37): These endorsements allow liability protection to flow upstream. They extend your general liability coverage to protect the project owner, while requiring the same endorsements from your subcontractors extends their coverage to protect you. This chain of risk transfer for both ongoing and completed operations is a standard requirement in almost all modern construction contracts.

- Per Project Aggregate (CG 25 03): This applies your general aggregate limit separately to each specific project, preventing a massive claim for ongoing operations on one jobsite from draining the aggregate coverage you need for another.

» Read More: Best General Liability Insurance Companies for Contractors

What Is Professional Liability Insurance for Contractors?

Professional liability insurance covers losses tied to professional negligence, design errors, and construction management failures. A standard professional liability policy is built to cover the brainwork of construction, acting as the financial backstop when your advice, coordination, or management causes harm.

Coverage & Policy Triggers

Unlike general liability, which is typically written on an occurrence basis, professional liability is typically written on a claims-made basis. It is triggered when a third party (like a project owner) makes a formal demand for money or files a lawsuit against you alleging a professional error. The policy is specifically designed to fill two massive gaps left by a standard general liability policy:

- It covers pure financial loss. If a construction manager fails to coordinate trades properly and a retail center opens six months late, the owner may pursue damages for lost rent and for extended financing costs. CGL won’t apply because there was no third-party bodily injury or tangible property damage to trigger coverage. Professional liability is the policy designed to respond to economic damages tied to management decisions.

- It addresses the professional services exclusion. If a contractor’s value-engineering recommendation contributes to a roof collapse, the GL carrier could deny the claim because the damage arose from a professional design decision rather than field labor. Professional liability is intended to cover both the delay impacts and the physical damage tied to those professional errors (subject to policy terms, limits, and exclusions).

Key Exclusions

Just as general liability typically excludes professional services, standard professional liability strictly excludes faulty physical workmanship. If your framing crew simply builds a wall out of plumb because they read the tape measure wrong, a core professional liability policy will not cover the resulting damage. To a professional liability underwriter, that is a field labor mistake, not a design error.

Additionally, standard professional liability policies will not cover the direct, first-party cost to repair your own defective work, nor will they cover intentional fraud or prior knowledge (mistakes you knew about before you purchased the policy).

Common Endorsements & Policy Features

Because the line between “design” and “construction” is so blurred, professional liability has become standard for many general contractors and construction managers doing design-build, construction manager at risk (CMAR), BIM coordination, delegated design oversight, or any advisory work. To customize this protection, contractors rely on the modern bundle and specific endorsements:

- Contractors Errors & Omissions: This endorsement bridges the workmanship exclusion. It steps in to cover the costs to repair or replace your own faulty physical labor (property damage to ‘your work’), ensuring you have protection for the physical fix even if no physical accident occurred.

- Rectification & Mitigation: This first-party endorsement pays the direct costs to fix a discovered design or engineering error before it turns into a massive third-party lawsuit. It is a vital feature that pays you directly to rebuild the mistake, providing an alternative to the traditional liability claim process.

- Protective Indemnity: If you hire a design professional (like an architect) and their own insurance limits are not high enough to cover a catastrophic mistake they made on your project, this feature allows your professional liability policy to step in and cover the shortfall.

Even when the design originates elsewhere, a contractor’s recommendations, shop drawing review processes, coordination decisions, and model inputs can create professional exposure, particularly when the owner treats the contractor as the single point of responsibility. These bundled features ensure there are no gaps in that responsibility.

» Read More: Best Professional Liability Insurance for Contractors

Why Design-Build Firms & Construction Managers Need Both

Design-build firms and construction managers often need both general liability and professional liability, as modern delivery models blend design responsibility with field execution.

In the traditional design-bid-build model, architects and contractors operate in separate lanes: the architect designs, the contractor builds, and the owner manages the handoffs. In design-build, the design-build entity takes responsibility for construction and for ensuring the design and coordination meet the professional standard of care.

Industry data reflects this shift toward alternative delivery. Design-build has steadily captured more market share, and according to industry projections, it is expected to account for nearly half of spending within certain construction segments, such as non-residential building, manufacturing, and infrastructure, by 2028. That trend pushes more contractors into design-related risk, sometimes without realizing how their scope reads in a dispute.

From an owner’s perspective, integrated delivery also simplifies claims. If a structural issue shows up, the owner often won’t spend months sorting out whether it’s design or construction. They’ll file against the single entity responsible for performance. That’s where a coverage gap can open if the contractor only carries one type of policy:

- CGL may deny the claim because it involves professional services.

- Professional liability may not be in place to cover the design-related exposure.

When that happens, the contractor can end up uninsured in the middle of a major dispute. Because of this, many private owners and public agencies require both policies in their contracts. And on projects where failures involve physical damage plus allegations of negligent design, coordination, review, or management, it’s common for both lines of coverage to get implicated.

BIM, AI & the Expanding Definition of Contractor Services

Technology is also pushing contractors further into professional territory. With BIM and AI-assisted tools, contractors increasingly influence decisions that affect the design itself. For example, contractors may use software to:

- Recommend design alternatives

- Optimize structural design or MEP routing

- Adjust layouts during value engineering

- Resolve clashes during BIM coordination

Historically, insurers might argue that these model-driven changes are professional decisions, not jobsite accidents. By 2026, many carriers have made that position explicit. It’s increasingly common to see “Generative AI” or “Absolute AI” exclusions and AI-related limitations layered into general liability and professional liability policies.

To keep coverage in place (or to get the right professional liability terms), underwriters now often ask how your firm controls AI outputs. They want to see human-in-the-loop review and documentation. If your firm lets autonomous tools change building integrity, code compliance, or system performance without documented human review, you should expect tougher underwriting and a much higher chance that one or both policies won’t respond to the resulting physical or financial loss.

Preconstruction Advice Can Create Professional Liability

The expanding role of general contractors also increases exposure. Many GCs now provide preconstruction services, including:

- Feasibility assessments

- Constructability reviews

- Procurement strategy

- Cost and scheduling advice

- Coordination between design disciplines

If that advice is wrong, the resulting loss can be framed as professional negligence. For services involving cost, scheduling, or procurement, a general liability policy will typically deny the claim because CGL insurance only covers physical property damage or bodily injury, not pure financial losses. When advice leads to physical failure—such as a building settling due to faulty foundation guidance—coverage often depends on the specific exclusion in place.

While broad professional exclusions may deny such claims, many contractors utilize limited exclusions (like the ISO CG 22 80 endorsement we discussed earlier) that preserve coverage for third-party bodily injury or property damage when professional services are provided in connection with the contractor’s own construction work. However, because CGL policies still typically exclude damage to the contractor’s own work, firms risk paying for structural repairs and legal defense out of pocket for project-related failures unless they carry a dedicated professional liability policy.

Delegated Design & Vicarious Liability

Risk increases sharply when a contractor delegates design work to subcontractors or outside consultants. Many contractors assume that if they don’t stamp drawings, they can’t be held responsible for design errors. Under single-point responsibility contracts (common in design-build), the owner may still hold the prime accountable for the entire project’s performance, regardless of who drew the plans.

If an engineer you hired makes a math error, you can have vicarious liability. In practical terms, the owner treats the consultant’s mistake as your problem because you’re the party with the main contract. And if that consultant is underinsured, has an exclusion, or lets their policy lapse, you can be left funding a professional claim you didn’t personally create. This is exactly where the protective indemnity feature of a contractors professional liability policy steps in to address the errors of the downstream parties you hired.

GL vs. PL: Real-World Construction Scenarios

The quickest way to understand the boundary is to look at how real claims get categorized. Carriers and attorneys don’t label a claim “GL” or “PL” solely based on your job title. They focus on the alleged cause of loss and the types of damages being claimed. Small facts in the timeline can flip which policy responds.

Before you work through the examples, it’s worth taking a hard look at your own contract language and scope. The Contractor’s Insurance Gap Analysis Checklist can help you review delegated design obligations, BIM responsibilities, value engineering language, and indemnity clauses that quietly create professional liability exposure.

Scenario 1: Accident vs. Calculation Error

This scenario highlights the difference between a jobsite accident and a failure of professional judgment.

- Incident: A contractor is tasked with installing a heavy custom mezzanine for a warehouse client.

- General Liability Event: During the lift, a subcontractor’s crane cable snaps, dropping a steel beam that crushes a client’s delivery truck parked nearby and injures a bystander. Because this is a sudden, accidental occurrence causing third-party bodily injury and property damage, the general liability policy responds to the truck and medical claims.

- Professional Liability Event: Instead of an accident, the contractor proposes a change to the mezzanine’s support structure to save the owner money. A year later, the mezzanine begins to sag because the revised design failed to account for the machinery’s weight. Because the root cause was a bad professional recommendation (design error) rather than a site accident, the contractor must rely on professional liability insurance to cover the resulting damage. However, because standard professional liability policies often focus on third-party economic loss and exclude the cost of fixing the contractor’s own work, a specific faulty workmanship or rectification endorsement (if the error were discovered during construction) would typically be required to cover the direct costs of the teardown and the rebuild.

Scenario 2: Site Mishap vs. Scheduling Error

This scenario shows how two different errors on the same project can require completely different policies.

- Incident: A construction manager is overseeing a new retail center. During the final push toward the grand opening, two unrelated issues occur.

- General Liability Event: While moving materials for a tenant fit-out, a forklift driver clips a water main, flooding a neighboring shop that is already open for business. Because this is a sudden, physical accident causing third-party property damage, the general liability policy triggers coverage for the shop’s ruined inventory and cleanup.

- Professional Liability Event: At the same time, the construction manager fails to coordinate the elevator technicians with the flooring subcontractors. This scheduling error pushes the entire project’s grand opening back by three months. There is no physical damage from this delay, just a $500,000 claim from the owner for lost rent. Because the scheduling error does not qualify as an occurrence (accident) and falls under professional services exclusions, general liability coverage is not triggered. Professional liability is the coverage designed for this type of pure economic loss.

Scenario 3: Design Error Chain Reaction

This scenario illustrates how general liability and professional liability work together when a subcontracted design error causes physical damage after a project is completed.

- Incident: A design-build contractor hires an outside electrical engineer to design a high-voltage system. The engineer makes a coordination error, placing a high-heat component too close to flammable insulation. Eventually, a fire breaks out, destroying the electrical room and shutting down the facility for a month.

- General Liability Event: Because the physical damage (the fire) occurred after the project was finished, it falls under the “products-completed operations” portion of the CGL policy. Furthermore, design-build contractor policies typically include a specific endorsement (CG 22 80) that provides a limited exclusion, ensuring that professional services performed in connection with your construction operations (including those performed by subcontractors) are not excluded. Because of this, the general liability policy will typically cover the physical fire damage to the building, even though the root cause was a design error.

- Professional Liability Event: While the general liability policy covers the physical fire damage (and the resulting loss of use damage), it will generally exclude pure economic losses that are not tied to physical damage. This is where the contractor’s professional liability policy steps in. It covers pure financial damages—such as the cost of remedial design or delay-related expenses—caused by the engineer’s error, and it protects the contractor if the at-fault engineer’s own insurance limits are not high enough to cover the total cost of the disaster.

The Modern Contractor’s Coverage Map

- Workers’ Compensation: For your people.

- General Liability: For the public’s people and property.

- Builders Risk: For the project itself during construction.

- Professional Liability: For your advice, designs, and management decisions.

Cost Comparisons & Factors for Contractors

Although general liability and professional liability pricing both start with revenue and claims history, underwriters look at different drivers when they build the final premium.

General Liability Pricing

Because CGL covers physical accidents, underwriters focus on what correlates with jobsite activity. The cost of GL insurance policies are commonly driven by gross sales, payroll, subcontractor costs, and trade class (for example, higher-risk excavation vs. lower-risk interior finishing). Carriers also weigh five-year claims history and subcontractor management practices. In the 2026 market, general liability pricing has begun to stabilize, though rates remain influenced by the increasing severity of bodily injury lawsuits and “nuclear verdicts.”

Professional Liability Pricing

Professional liability underwriters focus on the level of design responsibility and professional decision-making you accept. Beyond revenue and claims history, premiums are driven by project delivery (especially your design-build percentage), whether you employ in-house design professionals, and your project types. For example, multi-family residential often draws higher professional liability pricing than standard commercial work, because defect claims can be frequent and expensive.

General vs. Professional Liability Price Comparison

| Feature | General Liability | Professional Liability |

|---|---|---|

| What It Prices | Ongoing operations, completed operations, and physical exposure | Contractual responsibility and professional judgment |

| Primary Rating Factors | Revenue, claims history, payroll, subcontractor costs, and specific trade class | Revenue, claims history, design-build ratio, and project types |

| Market Volatility (2026) | Moderate (pressured by “nuclear verdicts” but seeing stabilized pricing) | Firming (driven by rising claim severity and defense costs) |

| Typical Premium Range (Small to Mid-Size Firm) | $1,000 – $50,000+ | $1,000 – $25,000+ |

Securing Your Business & Closing the Gaps

The most common misconception in contractor insurance is assuming CGL will respond whenever there’s a construction problem. General liability is the foundation for site-level accidents, but it’s not meant to cover professional judgment calls, such as design decisions, coordination failures, or advice that causes financial harm. That’s the lane professional liability was built for.

If your firm does design-build, CMAR, BIM coordination, or value engineering, relying on CGL alone is a financial gamble. Contracts have changed, owner expectations have changed, and in 2026, the tools contractors use every day can push them into “professional services” territory even when nobody set out to take on design responsibility.

The Modern Contractor’s Combined Risk Profile

A contractor’s risk profile now includes both physical safety and professional accuracy. When a dispute turns into litigation, the label on your business card won’t decide what you did. Your scope, your contract, your communications, and your deliverables will.

Carrying both coverages gives you a workable safety net across common claims, from third-party injuries to allegations that your scheduling or design coordination caused a costly delay. It also signals to owners and lenders that your firm can withstand a complicated claim without becoming financially unstable.

Next Steps: Auditing Your Current Coverage

A practical coverage audit starts with your CGL exclusions, especially professional services language and any 2026 ISO generative AI endorsements, and then works outward to your contracts. Look for delegated design obligations, BIM model responsibilities, value engineering authority, and clauses that require you to ensure code compliance or performance outcomes.

Once you’ve identified the pressure points, use the Contractor’s Insurance Gap Analysis Checklist below to prioritize fixes, then talk with a broker who routinely places contractor GL and E&O. The goal isn’t to buy every endorsement available. It’s to align your policies with how you actually build, and how your contracts say you build, so an office-side mistake doesn’t turn into a company-threatening loss.

Frequently Asked Questions about General Liability & Professional Liability

How are legal defense costs handled differently between General and Professional Liability?

The biggest financial difference is how attorney fees impact your available money. Standard General Liability defense costs are usually “outside the limits,” meaning the carrier pays your legal fees separately and leaves your full $1,000,000 limit available for the settlement. Professional Liability is typically written with “shrinking limits” (or “inside the limits”). This means every dollar spent on attorney fees and expert witnesses is deducted directly from your policy limit, leaving you with less money to actually pay the final judgment.

Will professional liability insurance cover a bidding or estimating error?

No. Neither General Liability nor Professional Liability will cover a purely economic bidding mistake (such as an estimator missing a zero on a spreadsheet or failing to account for material price inflation). Insurers categorize estimating errors, cost overruns, and failures to secure financing as uninsurable “commercial business risks,” not professional negligence. Professional liability only covers financial loss that directly results from negligent design, engineering, scheduling, or construction management.

Do artisan subcontractors (like plumbers or electricians) need professional liability insurance?

It depends entirely on the project delivery method. If a trade subcontractor is strictly executing “plan-and-spec” work (building exactly what the architect drew), General Liability is usually sufficient. However, if the subcontractor engages in “design-assist” contracts, routes their own MEP systems, or stamps their own shop drawings, they have crossed into professional services. In these cases, General Contractors will increasingly require the subcontractor to carry their own Contractors Professional Liability (CPrL) policy.

What is a “Retroactive Date” and why does it matter when switching policies?

Because Professional Liability is a “claims-made” policy (meaning you must have an active policy when the lawsuit is filed), it contains a Retroactive Date (or “Retro Date”). This is the exact date your very first PL policy began. If you switch insurance carriers, you must secure “Prior Acts” coverage to maintain that original Retro Date. If you fail to do this, your new policy will not cover any mistakes you made on projects completed before the new policy started, leaving you entirely uninsured for past work.

Can I buy professional liability insurance for just one specific construction project?

Yes. While General Liability is typically purchased as a blanket annual policy with a per-project aggregate, contractors can purchase a Project-Specific Professional Liability (PSPL) policy for a single high-risk job. A PSPL policy covers the entire design and construction team (including the prime, architects, and engineers) under one shared limit. It also typically includes an Extended Reporting Period (ERP) that keeps coverage active for 3 to 10 years after the project is completed to cover latent defects.

References & Additional Resources

- Design-Build Institute of America (DBIA). An industry authority on modern construction delivery methods providing market data that illustrates how the rise of design-build contracts is forcing general contractors to take on both physical construction risks and professional design exposures simultaneously.

- Dodge Construction Network. A leading provider of commercial construction market data and analytics tracking the project delivery trends that drive the necessity of bundled contractors professional liability (CPrL) policies.

- International Risk Management Institute (IRMI). An educational and analytical resource for risk management, offering extensive glossaries, reference materials, and expert analysis on construction insurance coverages, exclusions, and case law.

- Insurance Services Office (ISO). The advisory organization responsible for developing and publishing the standard commercial general liability policy forms and endorsements used by the majority of the property and casualty insurance industry.

- Occupational Safety and Health Administration (OSHA). Federal agency that maintains regulatory databases for workplace safety violations and incident records relevant to contractor operational risk.

Related Posts

What Is Contractor General Liability Insurance? (Complete Guide)

Contractor general liability insurance is required coverage that protects your business by paying for third-party injuries, property damage, and related…

How Much Does General Liability Insurance Cost for Contractors in 2026?

A standard $1M/$2M general liability policy for a small-to-mid-sized contractor typically costs between $750 and $2,500 annually. Your company's general…

What Does Contractor General Liability Insurance Cover?

Contractor general liability insurance covers financial losses resulting from third-party bodily injury, third-party property damage, advertising injury, and damages arising…

General Liability Insurance Requirements for Contractors

While state licensing boards may only require $50,000 to $100,000 in general liability coverage for contractors, most commercial construction contracts…

The Best Errors & Omissions Insurance Companies for 2026

The best errors and omissions (E&O) insurance companies for 2026 are Hiscox (Best Overall), ERGO Next (Best Customer Experience), and…